No-Code Crypto Strategy Builder: Visual Indicator Logic

Most traders have legitimate strategy ideas. They know that RSI below 30 after a 200-EMA cross is a structurally interesting setup. They know that ATR widens before breakouts. They know that volume confirming a reversal matters more than the reversal alone. The bottleneck has never been the idea — it's the gap between knowing what you want and writing 80 lines of pandas to express it. The Visual Strategy Builder closes that gap. Indicator nodes, comparison operators, AND/OR/NOT logic trees, all visual, all generating Freqtrade-compatible Python automatically.

What Is the No-Code Visual Strategy Builder

The Visual Strategy Builder is a drag-and-drop interface for creating algorithmic trading strategies — connecting condition nodes, picking indicators, defining entry/exit logic — without writing Python.

Internally, every visual configuration compiles to a real Freqtrade strategy class with populate_indicators, populate_entry_trend, and populate_exit_trend methods. You never have to read or edit that code unless you want to. When you do want to (custom callbacks, advanced DCA logic, machine-learning models), one click ejects to Code Mode with the visual configuration pre-rendered as Python.

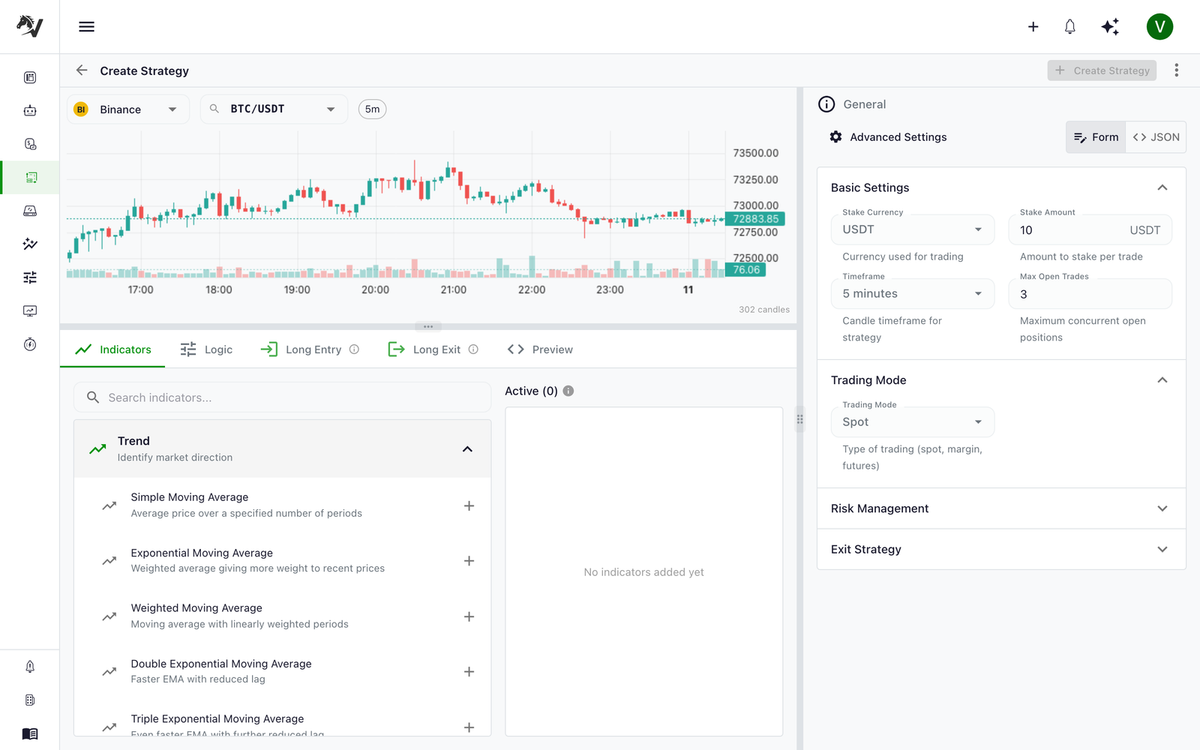

The builder lives on a single screen split into three regions: a live candlestick chart of the pair you're designing against (top-left), the indicator library and signal editor (lower panel), and a settings panel on the right covering trading mode, risk management, and exit behavior. Five tabs walk you through the full configuration:

How the Crypto Strategy Builder Works

Step 1: Choose Your Indicators

Pick from 25+ built-in technical indicators organized by category:

Trend

- Simple Moving Average (SMA), Exponential Moving Average (EMA)

- Weighted MA, Double EMA, Triple EMA, Kaufman Adaptive MA

Momentum

- RSI, MACD, Stochastic, Stochastic RSI

- Williams %R, CCI, Momentum, Rate of Change

Volatility

- Bollinger Bands, ATR, Keltner Channel

Volume

- OBV, MFI, CMF, Accumulation/Distribution

Trend confirmation / structure

- ADX, VWAP, Ichimoku Cloud, Parabolic SAR, Supertrend

Each indicator is fully configurable — period, multiplier, standard deviation, smoothing factor, anything the underlying TA-Lib function exposes. Deeper dives on the most common ones live in dedicated posts: RSI mean reversion, EMA crossover trend following, MACD strategy guide, Bollinger Bands strategy, and ATR stop-loss strategy.

Step 2: Define Entry Conditions

Build entry logic as a tree of conditions. The example below reads as: "Enter long when RSI is oversold AND price is above the 200 EMA AND MACD has just crossed over its signal line."

Logic node types available:

- AND — all child conditions must be true

- OR — at least one must be true

- NOT — invert a child condition

- COMPARE — compare two values with

>,<,=,>=,<=,!= - CROSSOVER / CROSSUNDER — detect indicator crosses on the current candle

- IN_RANGE — check whether a value falls between two bounds

Step 3: Define Exit Conditions

Same visual primitive, applied to position exits:

Take-profit and stop-loss are handled separately as risk-management settings, so exit conditions are usually about signal-driven exits (e.g., "the trend reversed") rather than risk-driven exits (e.g., "we hit −5%").

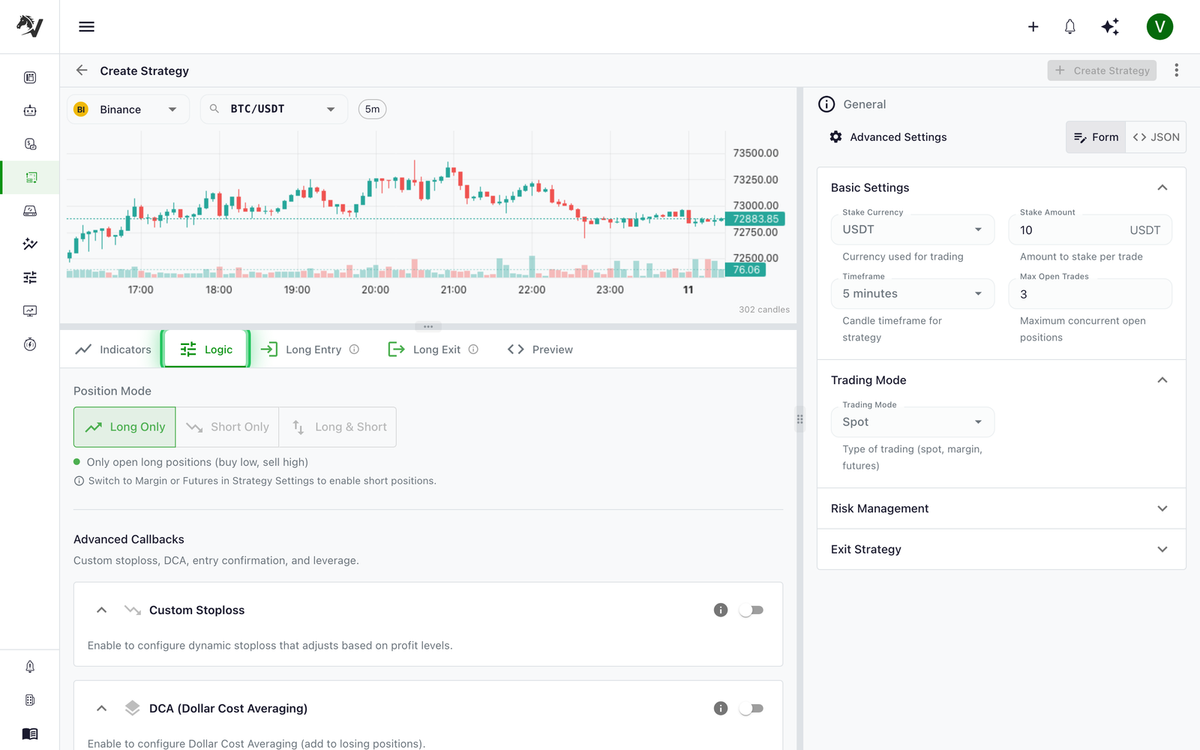

Step 4: Configure Position Management

The position-management settings panel covers the part of trading that isn't entry/exit signals:

- Leverage — fixed or dynamic, for margin/futures

- Stop-loss — fixed percentage or ATR-based

- DCA — dollar-cost-averaging ladders for DCA strategies

- Position mode — long-only, short-only, or both

All of this lives behind the Logic tab, alongside toggleable advanced callbacks for custom stoploss behavior, DCA ladders, leverage strategies, and confirmation checks before entry/exit:

Long/Short Strategies With Mirror Mode

For futures trading, the builder supports separate condition trees for long and short positions. Building both sides by hand is tedious — and a common source of bugs — so the builder also offers Mirror Mode: toggle it on and your long entry conditions are automatically inverted for shorts. The transformation is mechanical:

RSI < 30(long entry) →RSI > 70(short entry)CROSSOVERbecomesCROSSUNDER- Comparison operators flip (

>becomes<,>=becomes<=)

The full pattern, including when not to mirror, is in the long/short mirror mode post.

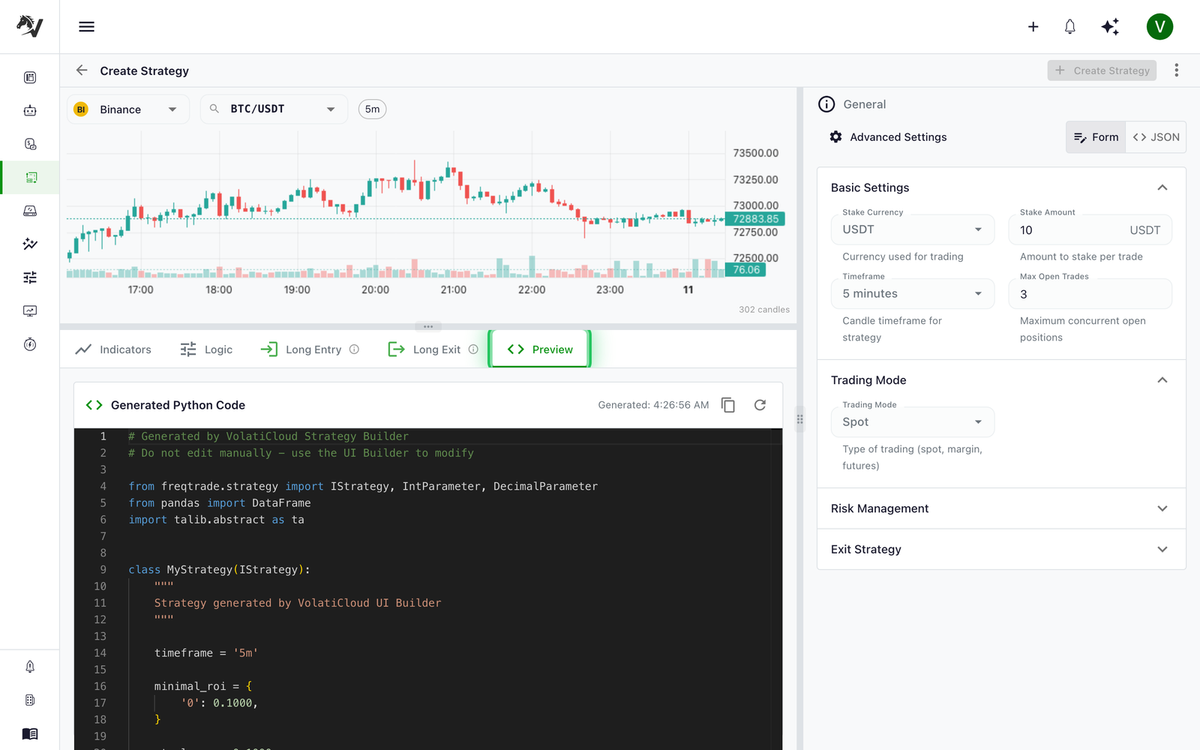

Preview the Generated Python Code

At any time, click the Preview tab to see the Python the visual configuration generates — rendered in a syntax-highlighted Monaco editor with proper freqtrade.strategy imports, typed parameters, and a fully-formed strategy class:

This is useful for:

- Learning Freqtrade strategy syntax by example

- Sanity-checking that the visual logic generates what you intended

- Sharing the strategy with technically-inclined teammates for review

- Migrating to Code Mode later without rebuilding from scratch

Ejecting to Code Mode for Advanced Logic

When you outgrow the visual layer — custom indicators, ML models, complex callbacks — eject to Code Mode:

- Click Eject to Code

- The generated Python opens in the in-app Monaco editor

- Continue developing with the full Freqtrade API:

custom_stoploss,confirm_trade_entry,adjust_trade_position,leverage,populate_indicatorswith TA-Lib or pandas-ta

Ejection is one-way for that strategy version. If you want to preserve the visual version for future edits, fork the strategy first — then eject the fork.

Real Example: RSI Mean Reversion With EMA Trend Filter

A practical starting point — RSI oversold with an EMA trend filter, the simplest robust mean-reversion configuration:

- Entry: Buy when

RSI(14) < 30ANDprice > EMA(200) - Exit: Sell when

RSI(14) > 70ORprice < EMA(50) - Stop-loss: −10% (or ATR-calibrated for the pair)

- Timeframe: 1h

Build this in the visual editor, preview the generated code, and run a backtest over 12+ months. If the metrics hold up, deploy it as a dry-run bot before going live. The paper trading to live promotion guide covers the full path.

Strategy Versioning and Forking

Once a backtest runs against a strategy, that strategy version becomes immutable — you can't silently change the conditions and pretend the old backtest still applies. To make changes, fork the strategy. Forking creates a new version that inherits the configuration, leaving the original (and all backtests against it) untouched. This is critical for:

- Comparing strategy variants against the same backtest period without confounds

- Maintaining an audit trail of which strategy version produced which trades

- Experimenting safely without losing a known-working baseline

The full versioning model is covered in the strategy versioning and forking post.

What the Builder Compiles To

For the technically curious, here's what a simple visual configuration compiles to in Code Mode:

from freqtrade.strategy import IStrategy

from pandas import DataFrame

import talib.abstract as ta

class RsiMeanReversion(IStrategy):

timeframe = '1h'

stoploss = -0.10

def populate_indicators(self, df: DataFrame, metadata: dict) -> DataFrame:

df['rsi'] = ta.RSI(df, timeperiod=14)

df['ema_200'] = ta.EMA(df, timeperiod=200)

df['ema_50'] = ta.EMA(df, timeperiod=50)

return df

def populate_entry_trend(self, df: DataFrame, metadata: dict) -> DataFrame:

df.loc[

(df['rsi'] < 30) & (df['close'] > df['ema_200']),

'enter_long'

] = 1

return df

def populate_exit_trend(self, df: DataFrame, metadata: dict) -> DataFrame:

df.loc[

(df['rsi'] > 70) | (df['close'] < df['ema_50']),

'exit_long'

] = 1

return df

The generated code is real Freqtrade Python — readable, exportable, and indistinguishable from hand-written code. There is no proprietary runtime layer between the builder and Freqtrade.

Try the Visual Strategy Builder�

Open the console, navigate to Strategies → New Strategy, and pick UI Builder mode. The Starter plan is free and the trial gives you Pro features for 7 days — enough to build a strategy, run backtests, and even try hyperparameter optimization.

Related guides

- UI Builder Guide — Full reference documentation for the visual strategy builder.

- Strategies Overview — Trading modes, position direction, and strategy concepts.

- Backtesting Overview — Validate your strategy against historical data before going live.